- 234 Balaclava Road, Caulfield North VIC 3161

- contactus@guests.com.au

- (03) 9509 7033

Oldest Buildings in the World.

Check out the oldest Buildings in the World.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

..

‘Renewed concerns’ about economy sees consumer sentiment dip: Westpac

Consumers remain deeply pessimistic about the near-term outlook for the economy despite signs of improvement last month, says the major bank.

.

The Westpac Consumer Sentiment Index fell 1.8 per cent to 84.4 in March with concerns still worried about the outlook for the economy.

Westpac said while there were promising signs last month that the consumer gloom that has dominated the past two years was beginning to lift, the March survey indicates that progress is “slow at best”.

“Consumers are still deeply pessimistic and becoming more concerned about the economy’s near-term outlook,” the Westpac Consumer Sentiment report stated.

The index indicated renewed concerns about the economic outlook.

Four of the five sub-indexes recorded declines in March, with the biggest move being a 4.5 per cent fall in the economic outlook.

The next biggest decline was the next 12 months sub-index which offset just over half of the gain from February.

“Assessments of family finances and ‘time to buy a major household item’ also retraced some of their February gains, with all still well below long run average levels despite some modest net improvement over the last six months,” Westpac said.

“The only positive was around the ‘economic outlook, next 5 years’ sub-index which edged up 1.1 per cent to be at 94, slightly above the long run average of 92.”

The major bank said responses to the survey suggest that sentiment made a sharp turnaround following the RBA decision.

“Sentiment amongst those surveyed prior to the decision came in at a much stronger 94.9 compared to 79.3 amongst those surveyed post-decision – almost identical to the swing recorded in February,” the report said.

“The implication is that while few would have been expecting rates to be cut, many consumers may have been hoping for a more positive message on inflation and the interest rate outlook.

“However, the RBA Governor was still not ruling out the possibility of further rate rises following the March meeting.”

Westpac Group senior economist Matthew Hassan said the RBA’s commentary looks to be tempering consumer expectations for interest rates as well, with fears of rate hikes easing but few expecting rate cuts any time soon.

The Westpac-Melbourne Institute Mortgage Rate Expectations Index, which tracks consumer expectations for variable mortgage rates over the next 12 months, dipped 0.5 per cent to 120.9.

“The mix of responses shows 40 per cent of consumers are still bracing for rate increases, 22 per cent expect no change, 22 per cent expect declines and 15 per cent simply “don’t know,” said Hassan.

Hassan said consumers remain relatively comfortable about the outlook for jobs, however.

“The Westpac-Melbourne Institute Unemployment Expectations Index rose slightly, by 1 per cent, in February but at 128.1 is still in line with the long run average of 129,” he said.

“Readings remain consistent with a softening in labour market conditions rather than a sharp rise in job losses.”

Housing-related sentiment improved slightly overall for the month with another lift in assessments of time to buy and price expectations holding at optimistic levels.

Miranda Brownlee

27 March 2024

accountantsdaily.com.au

A comprehensive list of guides to industry specific tax deductions.

The following is a list the ATO has compiled that is tailored to occupations and industries.

.

Use the table below to access either:

- the complete occupation or industry guide including income, expenses, record keeping and examples

- select the link in the left column of the table

- read the content online

- the PDF summary of common work-related expenses for your occupation or industry, you can

- select the link in the right column of the table to open the PDF

- you can download as a PDF.

UNDERPERFORMING EMPLOYEES: WHEN CAN YOU TERMINATE?

Terminating an underperforming employee requires caution. Employers must follow fair procedures to avoid legal issues such as unfair dismissal claims.

.

Firing an employee hastily or without proper procedures can lead to uncomfortable situations and damage the company's reputation. Regrettably, sometimes, management pressure means making uninformed decisions that open the company to risk.

Poor performance is perpetuated because employees are often unaware of their subpar performance, and their managers, for various reasons, fail to effectively address the situation by delaying action.

This article goes through the performance process, offering hints and tips for HR to support businesses in creating high-performing organisations while mitigating risk.

HOW HR CAN SUPPORT BUSINESSES

As trusted advisors, HR leaders often face the dilemma of doing the right thing while businesses prioritise expediency and cost-cutting measures, usually encouraged by senior management.

In certain circumstances, swift termination of an employee's employment can be advantageous, especially when immediate and decisive action aligns with the company's best interests. This approach may be driven by the perception that the business risks associated with retaining an employee outweigh the potential legal consequences employers might encounter by acting promptly.

However, this 'swift' approach should be the exception, not the norm. It is an essential reminder that high-performing organisations consistently engage in constructive discussions with their employees regarding their performance. They establish well-defined goals, offer feedback, and provide support to maximise employee productivity. In cases of underperformance, these organisations promptly take appropriate and sensitive measures to address the issue.

STEPS TO ADDRESS EMPLOYEE PERFORMANCE

1. Identify and assess the underperformance

- Write down examples of problematic behaviours or actions.

- Assess the seriousness, duration, and impact of the problem.

- Organise a meeting with the employee to discuss the issue.

2. Meet with the employee

- Describe the problem clearly and give specific examples of where they are not meeting expectations

- Explain the impact on the business, co-workers, and the employee's work.

3. Agree on a solution

- Explore ideas and suggest ways to fix the problem.

- Reinforce the value of the employee's role.

- Record the agreed actions in a performance improvement plan.

4. Monitor and review performance

- Follow through with the support offered and regularly check in.

- Have a follow-up meeting to review progress.

- Update the performance improvement plan as needed.

- Acknowledge the employee's progress and focus on remaining improvements.

DISMISSING AN EMPLOYEE FOR UNDERPERFORMANCE

If performance doesn't improve and a written warning has been issued, sometimes a dismissal is the next step. Termination of employment is a significant step that requires a valid reason related to the employee's capacity or conduct.

Employers must follow a fair performance management and dismissal process and avoid harsh, unjust, or unreasonable circumstances. Fairness is crucial, especially during termination, and employees should be provided with reasons for dismissal and an opportunity to respond.

Before dismissing an employee, employers should have taken the following steps:

- ensuring that the purpose of performance meetings has been communicated in advance and allowing the employee adequate time to prepare

- informing the employee of their right to have a support person present

- clearly outlining the expected performance level and required improvements.

- providing clear warnings about the need for performance improvement

- granting reasonable time and support to enhance performance

- expressing the possibility of dismissal if performance does not improve.

Before dismissing an employee, the employer must provide written reasons for considering dismissal and allow the employee a reasonable opportunity to respond. Any response from the employee must be considered before making a termination decision. Failure to follow these steps can result in a successful unfair dismissal claim against the employer.

Note: Businesses with fewer than 15 employees are subject to specific dismissal rules that differ from those applicable to larger organisations. During the first 12 months of employment, small business employees cannot claim unfair dismissal. However, if an employee is dismissed after this period and the employer has complied with the Small Business Fair Dismissal Code, the dismissal will be deemed fair.

Access the Small Business Fair Dismissal Code and checklist.

KEY LESSONS

Terminating an underperforming employee is a valid reason for termination. However, employers must follow specific steps to avoid landing in hot water. Some key takeaways are:

- Immediate Communication: If performance concerns arise, promptly address them with the employee through transparent and open communication.

- Documentation: Utilise tools like performance improvement plans. Document all conversations regarding performance, informal or formal, and maintain records of any written warnings given to the employee. This documentation can significantly benefit the organisation if an unfair dismissal claim arises.

- Procedural fairness: Ensure that any implemented performance management process adheres to the principles of procedural fairness.

Catherine Ngo

Content writer, presenter and podcaster

mybusiness.com.au

THE 2025 FINANCIAL YEAR TAX & SUPER CHANGES YOU NEED TO KNOW!

The new financial year is fast approaching and so are a number of changes to superannuation contribution amounts and the individual tax rates. These changes are outlined below, as is some information on how you may be able to work with these changes when managing your tax affairs during 2024-25.

.

Superannuation

From 1 July 2024, the amount you can contribute to super will increase.

The amount you can contribute to superannuation will increase on 1 July 2024 from $27,500 to $30,000 for concessional super contributions and from $110,000 to $120,000 for non-concessional contributions.

For those with the disposable income to contribute, superannuation can be very attractive with a 15% tax rate on concessional super contributions and potentially tax-free withdrawals when you retire. For business owners who might have had an exceptional year or sold their business, it's an opportunity to get more into super. However, the timing of contributions will be important to maximise outcomes.

If you know you will have a capital gains tax liability in a particular year, you may be able to use ‘catch up’ contributions to make a larger than usual contribution and use the tax deduction to help offset your capital gain tax bill. But, this strategy will only work if you meet the eligibility criteria to make catch up contributions and you lodge a Notice of intent to claim or vary a deduction for personal super contributions, with your super fund.

Using the bring forward rule

This topic has been touched on in previous articles but the ‘bring forward rule’ enables you to bring forward up to 2 years’ worth of future non-concessional contributions into the year you make the contribution – this is assuming your total superannuation balance enables you to make the contribution and you are under age 75.

If you utilise the bring forward rule before 30 June 2024, the maximum that can be contributed is $330,000. However, if you wait to trigger the bring forward until on or after 1 July 2024, then the maximum that can be contributed under this rule is $360,000.

‘Catch up’ contributions

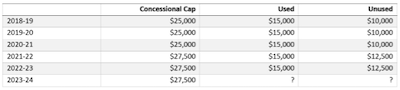

If your super balance is below $500,000 prior to 30 June, and you want to quickly increase the amount you hold in super, you can utilise any unused concessional super contributions amounts from the last 5 years.

For example, a taxpayer has only been using $15,000 of the concessional super cap for the last few years. The super balance at 30 June 2023 was $300,000, so this person is well within the limit to make catch up contributions.

This person could access their $27,500 concessional cap for 2023-24 plus the unused $55,000 from the prior 5 financial years.

However, if the unused amount from 2018-19 is not used by 30 June 2024, the $10,000 will no longer be available.

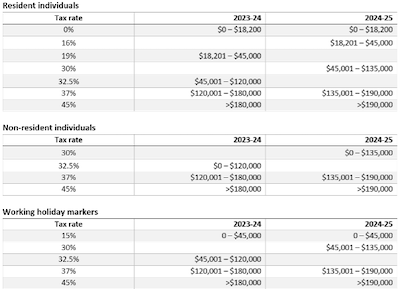

Taxation

As we all know, the revised stage 3 tax cuts have passed Parliament and will come into effect on 1 July 2024. The following table outlines what the rates currently are and what they will be from the 2025 financial year.

Salary sacrifice agreements should be checked before the new tax rates come into effect to ensure they will continue to produce the result you are after.

Be sure to contact us if you have any concerns or questions.

Small business benchmarks

The ATO has developed quite a number of benchmarks to help small businesses develop an idea of their performance compared to similar businesses in the same industry.

.

The link below takes you to the A-Z list of benchmarks and covers a large number of small businesses. Such a comparison can be a very helpful when looking for ways to improve your business’s profitability and productivity.

Call us if you have any questions.

A-Z list of benchmarks.

ATO’s debts on hold campaign prompts new IGTO guidance

New guidance has been released on best practice principles for debt notifications in response to the re-activation of old debts by the ATO.

.

The Inspector-General of Taxation Ombudsman, Commonwealth Ombudsman and ACT Ombudsman have published a report advising government agencies about how to tell people they owe money to the government.

The report has been issued off the back of community concerns that were raised last year regarding the ATO’s approach to debt collection.

The ATO issued tens of thousands of letters both to tax agents and individuals in 2023, advising them that previous debts on hold that had been written off as “uneconomic to pursue” would be revived and offset against clients’ tax refunds or credits.

The report explained that notifications about debt to individuals can be a “worrying, traumatic and confusing experience” and can negatively affect people’s wellbeing.

“The impact of being told you owe the government a debt can be increased if the debt is unknown, it’s old, it’s unexpected, or if there is limited information about the reasons for the debt, who to contact for more information or how to challenge the debt, who to contact for more information or how to challenge the debt,” the report stated.

It acknowledged that while agencies must act and are expected to act per the law, they are also obliged to help people and act in the best interests of the Australian community.

“While the law may require agencies to take certain action, agencies are also responsible for determining how they take that action in a way that minimises distress to affected and impacted people,” the guidance stated.

Inspector-General and Taxation Ombudsman, Karen Payne, said the ATO was told by the Australian National Audit Office in 2023 that it needed to review its practice concerning debts classed as “uneconomical to pursue” which is what led the Tax Office to send out letters advising of the debts.

“Now, that didn’t necessarily mean that you should write to all taxpayers telling them that they owe these uneconomical to pursue debts, particularly where the ATO’s own online systems hadn’t caught up. So these [debts] looked invisible frankly to taxpayers,” Payne said, speaking to Accountants Daily.

“What the professional bodies said when they met with the ATO as part of their stewardship group was ‘Well, if you think this is a good idea, then you should tell people what debts they owe, including debts that are on pause, but don’t do that until it can be seen on your system’.

“[However], before the systems were updated to let people know what the debts were, so they could at least marry up what the communication was saying, the Tax Office was writing to people saying you owe these debts including debts of 20 cents. So the whole communication was handled poorly, frankly.”

Commonwealth Ombudsman Iain Anderson said the ATO was previously issued with a report back in 2009 before the IGTO office was established.

“The report contained a recommendation that the ATO should provide further information to taxpayers when the debt is raised including the source of the debt, how much interest has been charged and why it is be raised and how to obtain further information,” the Commonwealth Ombudsman said.

“They agreed or partially agreed to all the recommendations in that report.

“It’s been disappointing that they haven’t done that this time around.”

The Commonwealth Ombudsman said the issues raised in the report are relevant to a whole range of government departments, beyond just the ATO.

“A lot of government departments need to chase debts and a lot of them have issues with how well they communicate with people,” he stated.

“They need to stake steps to put people at the centre of how they do things.”

Individuals need to know what a debt is, where it has come from, particularly where the department is chasing down an old debt, said Anderson.

“The first thing someone does when they get a letter from a government agency saying that they owe money is what have I done? Have I missed something? That’s where an apology really comes in or an explanation to say where the debt comes from and why it’s now being pursued,” he stated.

It is also important that individuals are properly informed so that they can pursue remedies such as contesting the debt, he added.

“Communicating clearly goes beyond chasing debt, it’s something that government agencies need to get much better at.”

The IGTO said that one of the most concerning scenarios concerning debts previously on hold is that taxpayers have limited opportunity to enter payment arrangements.

Payne explained that where the taxpayer has entered into a payment arrangement with the ATO, the Commissioner of Taxation does have the discretion not to automatically offset the debt against the refund.

“The key issue here is that if you’ve got one of these uneconomical to pursue debts and you don’t know that you owe the debt and it is not visible on the ATO’s systems that you owe the debt, then you’re not going to be thinking about entering into a payment arrangement because you don’t even know you have it,” she stated.

“So what we would encourage the Tax Office to think about is that prior to doing the automatic offsetting, tell people that they owe the debt, see if they need to enter into some kind of payment arrangement or payment instalments so that they can at least take the benefit of the discretion that the Commissioner has not to automatically offset these debts.”

Miranda Brownlee

26 March 2024

accountantsdaily.com.au

Illegal access nets $637 million

The ATO has found $637 million of superannuation savings has left the system due to illegal early access carried out through SMSFs.

.

The figures were released by the regulator today at the SMSF Association National Conference 2024 in Brisbane, where ATO superannuation and employer obligations deputy commissioner Emma Rosenzweig provided the first report on an illegal early access estimate project revealed late last year.

“I’m here today to announce for the first time that we have found for the 2019/20 year an estimated $381 million of super has been illegally withdrawn by trustees of SMSFs,” Rosenzweig said.

“This figure would have been half-a-billion dollars if we hadn’t protected over $125 million leaving the system as part of our new registrant program.

“In the 2020/21 year, we estimate over $256 million of super has been illegally accessed, with almost $170 million additional that was protected at registration.”

“These are large amounts of money and they don’t include prohibited loans across those two years, so a total of $637 million of superannuation savings has left the system illegally through SMSFs.”

She added prohibited loans were also of concern and in each of the two financial years mentioned, SMSFs entered into more than $200 million in prohibited loans each year, but 75 per cent were repaid.

Newly established SMSFs were more likely to engage in illegal early access or prohibited loans compared to established funds and around two-thirds of the $930 million involved in illegal access or loans over the two years came from people entering the system with no genuine intention to run a fund, she noted.

She said the ATO formed its estimate using audit reports and examining funds that had yet to lodge an annual return and would continue to do so each year as the regulator remained concerned illegal early access was ongoing.

“We looked at all auditor contravention reports of funds that have lodged in those two years where those reports had noted a contravention that could amount to illegal early access and then for those SMSFs that have not lodged, we undertook a random inquiry program and a statistically valid sample,” she said.

“Through the results of both of those we have come up with this estimate across the entire population.

“So will we be doing it every year? Yes.

“We do see already in 2021/22 there are indicators that suggest that illegal early access is still prevalent. We continue to see many new trustees entering into the system with the sole intent of raiding their retirement savings, sometimes facilitated by promoters charging a large fee.”

Jason Spits

February 21, 2024

smsmagazine.com.au

Countries producing the most solar power by gigawatt hours

Check out the countries that produce the most solar power.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Sharing economy reporting regime for platform operators

Individuals participating in the sharing economy should be aware that transactions for supplying taxi travel/ride sourcing and short-term accommodation are now required to be reported under the sharing economy reporting regime (SERR).

.

That reporting requirement will be expanded for 2024-25 year.

Generally, all operators of electronic distribution 2023–2024 income year must report transactions made through their platform.

However, from 1 July 2024, the SERR will apply to all other reportable transactions of electronic distribution platforms operators, including hiring of assets (consisting of hire of personal assets, storage or business space), food delivery and professional performing tasks and activities will need to be reported.

Latest Industry News

‘Renewed concerns’ about economy sees consumer sentiment dip: Westpac

Consumers remain deeply pessimistic about the near-term outlook for the economy despite signs of improvement...

A comprehensive list of guides to industry specific tax deductions.

The following is a list the ATO has compiled that is tailored to occupations and industries. . Use the...

UNDERPERFORMING EMPLOYEES: WHEN CAN YOU TERMINATE?

Terminating an underperforming employee requires caution. Employers must follow fair procedures to avoid legal...

THE 2025 FINANCIAL YEAR TAX & SUPER CHANGES YOU NEED TO KNOW!

The new financial year is fast approaching and so are a number of changes to superannuation contribution...

The ATO has developed quite a number of benchmarks to help small businesses develop an idea of their...

ATO’s debts on hold campaign prompts new IGTO guidance

New guidance has been released on best practice principles for debt notifications in response to the...

Illegal access nets $637 million

The ATO has found $637 million of superannuation savings has left the system due to illegal early access...

Countries producing the most solar power by gigawatt hours

Check out the countries that produce the most solar...

Sharing economy reporting regime for platform operators

Individuals participating in the sharing economy should be aware that transactions for supplying taxi...

Why employee v contractor comes down to fine print

The task of worker classification has been a long-running point of contention but the Commissioner’s...

Australian Taxation Office (ATO) shifting to firmer debt collection activity

The ATO has flagged a return to more aggressive debt collection actions after seeing a trend of profitable...

Latest Guests News

We are pleased to supply you with the latest edition of Client Alert, which contains information on a number...