- 234 Balaclava Road, Caulfield North VIC 3161

- contactus@guests.com.au

- (03) 9509 7033

THE 2025 FINANCIAL YEAR TAX & SUPER CHANGES YOU NEED TO KNOW!

The new financial year is fast approaching and so are a number of changes to superannuation contribution amounts and the individual tax rates. These changes are outlined below, as is some information on how you may be able to work with these changes when managing your tax affairs during 2024-25.

.

Superannuation

From 1 July 2024, the amount you can contribute to super will increase.

The amount you can contribute to superannuation will increase on 1 July 2024 from $27,500 to $30,000 for concessional super contributions and from $110,000 to $120,000 for non-concessional contributions.

For those with the disposable income to contribute, superannuation can be very attractive with a 15% tax rate on concessional super contributions and potentially tax-free withdrawals when you retire. For business owners who might have had an exceptional year or sold their business, it's an opportunity to get more into super. However, the timing of contributions will be important to maximise outcomes.

If you know you will have a capital gains tax liability in a particular year, you may be able to use ‘catch up’ contributions to make a larger than usual contribution and use the tax deduction to help offset your capital gain tax bill. But, this strategy will only work if you meet the eligibility criteria to make catch up contributions and you lodge a Notice of intent to claim or vary a deduction for personal super contributions, with your super fund.

Using the bring forward rule

This topic has been touched on in previous articles but the ‘bring forward rule’ enables you to bring forward up to 2 years’ worth of future non-concessional contributions into the year you make the contribution – this is assuming your total superannuation balance enables you to make the contribution and you are under age 75.

If you utilise the bring forward rule before 30 June 2024, the maximum that can be contributed is $330,000. However, if you wait to trigger the bring forward until on or after 1 July 2024, then the maximum that can be contributed under this rule is $360,000.

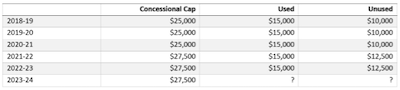

‘Catch up’ contributions

If your super balance is below $500,000 prior to 30 June, and you want to quickly increase the amount you hold in super, you can utilise any unused concessional super contributions amounts from the last 5 years.

For example, a taxpayer has only been using $15,000 of the concessional super cap for the last few years. The super balance at 30 June 2023 was $300,000, so this person is well within the limit to make catch up contributions.

This person could access their $27,500 concessional cap for 2023-24 plus the unused $55,000 from the prior 5 financial years.

However, if the unused amount from 2018-19 is not used by 30 June 2024, the $10,000 will no longer be available.

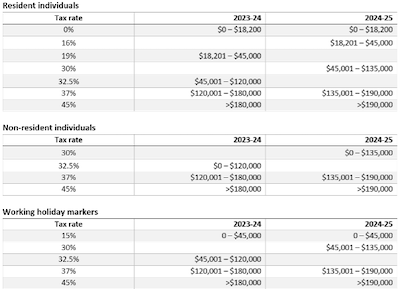

Taxation

As we all know, the revised stage 3 tax cuts have passed Parliament and will come into effect on 1 July 2024. The following table outlines what the rates currently are and what they will be from the 2025 financial year.

Salary sacrifice agreements should be checked before the new tax rates come into effect to ensure they will continue to produce the result you are after.

Be sure to contact us if you have any concerns or questions.

Small business benchmarks

The ATO has developed quite a number of benchmarks to help small businesses develop an idea of their performance compared to similar businesses in the same industry.

.

The link below takes you to the A-Z list of benchmarks and covers a large number of small businesses. Such a comparison can be a very helpful when looking for ways to improve your business’s profitability and productivity.

Call us if you have any questions.

A-Z list of benchmarks.

ATO’s debts on hold campaign prompts new IGTO guidance

New guidance has been released on best practice principles for debt notifications in response to the re-activation of old debts by the ATO.

.

The Inspector-General of Taxation Ombudsman, Commonwealth Ombudsman and ACT Ombudsman have published a report advising government agencies about how to tell people they owe money to the government.

The report has been issued off the back of community concerns that were raised last year regarding the ATO’s approach to debt collection.

The ATO issued tens of thousands of letters both to tax agents and individuals in 2023, advising them that previous debts on hold that had been written off as “uneconomic to pursue” would be revived and offset against clients’ tax refunds or credits.

The report explained that notifications about debt to individuals can be a “worrying, traumatic and confusing experience” and can negatively affect people’s wellbeing.

“The impact of being told you owe the government a debt can be increased if the debt is unknown, it’s old, it’s unexpected, or if there is limited information about the reasons for the debt, who to contact for more information or how to challenge the debt, who to contact for more information or how to challenge the debt,” the report stated.

It acknowledged that while agencies must act and are expected to act per the law, they are also obliged to help people and act in the best interests of the Australian community.

“While the law may require agencies to take certain action, agencies are also responsible for determining how they take that action in a way that minimises distress to affected and impacted people,” the guidance stated.

Inspector-General and Taxation Ombudsman, Karen Payne, said the ATO was told by the Australian National Audit Office in 2023 that it needed to review its practice concerning debts classed as “uneconomical to pursue” which is what led the Tax Office to send out letters advising of the debts.

“Now, that didn’t necessarily mean that you should write to all taxpayers telling them that they owe these uneconomical to pursue debts, particularly where the ATO’s own online systems hadn’t caught up. So these [debts] looked invisible frankly to taxpayers,” Payne said, speaking to Accountants Daily.

“What the professional bodies said when they met with the ATO as part of their stewardship group was ‘Well, if you think this is a good idea, then you should tell people what debts they owe, including debts that are on pause, but don’t do that until it can be seen on your system’.

“[However], before the systems were updated to let people know what the debts were, so they could at least marry up what the communication was saying, the Tax Office was writing to people saying you owe these debts including debts of 20 cents. So the whole communication was handled poorly, frankly.”

Commonwealth Ombudsman Iain Anderson said the ATO was previously issued with a report back in 2009 before the IGTO office was established.

“The report contained a recommendation that the ATO should provide further information to taxpayers when the debt is raised including the source of the debt, how much interest has been charged and why it is be raised and how to obtain further information,” the Commonwealth Ombudsman said.

“They agreed or partially agreed to all the recommendations in that report.

“It’s been disappointing that they haven’t done that this time around.”

The Commonwealth Ombudsman said the issues raised in the report are relevant to a whole range of government departments, beyond just the ATO.

“A lot of government departments need to chase debts and a lot of them have issues with how well they communicate with people,” he stated.

“They need to stake steps to put people at the centre of how they do things.”

Individuals need to know what a debt is, where it has come from, particularly where the department is chasing down an old debt, said Anderson.

“The first thing someone does when they get a letter from a government agency saying that they owe money is what have I done? Have I missed something? That’s where an apology really comes in or an explanation to say where the debt comes from and why it’s now being pursued,” he stated.

It is also important that individuals are properly informed so that they can pursue remedies such as contesting the debt, he added.

“Communicating clearly goes beyond chasing debt, it’s something that government agencies need to get much better at.”

The IGTO said that one of the most concerning scenarios concerning debts previously on hold is that taxpayers have limited opportunity to enter payment arrangements.

Payne explained that where the taxpayer has entered into a payment arrangement with the ATO, the Commissioner of Taxation does have the discretion not to automatically offset the debt against the refund.

“The key issue here is that if you’ve got one of these uneconomical to pursue debts and you don’t know that you owe the debt and it is not visible on the ATO’s systems that you owe the debt, then you’re not going to be thinking about entering into a payment arrangement because you don’t even know you have it,” she stated.

“So what we would encourage the Tax Office to think about is that prior to doing the automatic offsetting, tell people that they owe the debt, see if they need to enter into some kind of payment arrangement or payment instalments so that they can at least take the benefit of the discretion that the Commissioner has not to automatically offset these debts.”

Miranda Brownlee

26 March 2024

accountantsdaily.com.au

Illegal access nets $637 million

The ATO has found $637 million of superannuation savings has left the system due to illegal early access carried out through SMSFs.

.

The figures were released by the regulator today at the SMSF Association National Conference 2024 in Brisbane, where ATO superannuation and employer obligations deputy commissioner Emma Rosenzweig provided the first report on an illegal early access estimate project revealed late last year.

“I’m here today to announce for the first time that we have found for the 2019/20 year an estimated $381 million of super has been illegally withdrawn by trustees of SMSFs,” Rosenzweig said.

“This figure would have been half-a-billion dollars if we hadn’t protected over $125 million leaving the system as part of our new registrant program.

“In the 2020/21 year, we estimate over $256 million of super has been illegally accessed, with almost $170 million additional that was protected at registration.”

“These are large amounts of money and they don’t include prohibited loans across those two years, so a total of $637 million of superannuation savings has left the system illegally through SMSFs.”

She added prohibited loans were also of concern and in each of the two financial years mentioned, SMSFs entered into more than $200 million in prohibited loans each year, but 75 per cent were repaid.

Newly established SMSFs were more likely to engage in illegal early access or prohibited loans compared to established funds and around two-thirds of the $930 million involved in illegal access or loans over the two years came from people entering the system with no genuine intention to run a fund, she noted.

She said the ATO formed its estimate using audit reports and examining funds that had yet to lodge an annual return and would continue to do so each year as the regulator remained concerned illegal early access was ongoing.

“We looked at all auditor contravention reports of funds that have lodged in those two years where those reports had noted a contravention that could amount to illegal early access and then for those SMSFs that have not lodged, we undertook a random inquiry program and a statistically valid sample,” she said.

“Through the results of both of those we have come up with this estimate across the entire population.

“So will we be doing it every year? Yes.

“We do see already in 2021/22 there are indicators that suggest that illegal early access is still prevalent. We continue to see many new trustees entering into the system with the sole intent of raiding their retirement savings, sometimes facilitated by promoters charging a large fee.”

Jason Spits

February 21, 2024

smsmagazine.com.au

Countries producing the most solar power by gigawatt hours

Check out the countries that produce the most solar power.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Sharing economy reporting regime for platform operators

Individuals participating in the sharing economy should be aware that transactions for supplying taxi travel/ride sourcing and short-term accommodation are now required to be reported under the sharing economy reporting regime (SERR).

.

That reporting requirement will be expanded for 2024-25 year.

Generally, all operators of electronic distribution 2023–2024 income year must report transactions made through their platform.

However, from 1 July 2024, the SERR will apply to all other reportable transactions of electronic distribution platforms operators, including hiring of assets (consisting of hire of personal assets, storage or business space), food delivery and professional performing tasks and activities will need to be reported.

Why employee v contractor comes down to fine print

The task of worker classification has been a long-running point of contention but the Commissioner’s response to recent court cases suggests a written contract is king.

.

The classification of an individual as an employee or contractor for PAYG and superannuation obligations has been a long-running point of contention.

With the High Court decisions of Jamsek and Personnel Contracting changing the determination process, together with the recent case of JMC Pty Ltd v Commissioner of Taxation potentially expanding the role of the contractor, the question before us now is: where are we with the Commissioner’s response?

Background

In 2022, Jamsek and Personal Contracting determined that the terms and conditions of a written contract between parties were what was relevant when deciding whether an individual providing services is characterised as an employee or a contractor.

As a result, a written agreement between parties contains the determining factors in the employee v contractor issue (control, risk, integration of the individual into the principal’s business).

Provided the agreement is not a sham or has not been varied, it is not necessary for further facts and/or evidence to be gathered or considered by the parties in determining the outcome.

JMC Pty Ltd v Commissioner of Taxation [2023]

JMC was a superannuation case concerning whether sections 12(1) and 12(3) of the Superannuation Guarantee Administration Act 1992 applied to a contract primarily for labour.

The decision is important because including a term that allows for delegating or transferring someone's services in the written agreement will likely lead to them being characterised as a contractor instead of an employee.

The Full Federal Court clearly stated (paragraph 89):

“The right bestowed upon Mr Harrison to subcontract or assign the performance of his teaching services, subject to written consent, was a real and substantial right which was inconsistent with an employment relationship between him and JMC.”

This decision expands the potential for individuals to be engaged as contractors where their agreements have such a delegation authority, regardless of whether the principal approves the delegation. The fact that it exists is the primary issue.

This means that a principal may directly hire an individual for services without the need for any intermediary entity.

The Commissioner’s position

Taxation ruling TR 2023/4 outlines the Commissioner’s position.

It starts in a somewhat pedestrian fashion on the question “who is an employee” for PAYG, and reemphasises that it will be approached in a “holistic” manner.

But the key points in the ruling with respect to the question of employee v contractor are as follows:

- The delegation authority

The Commissioner accepts the position that a right to delegate or assign services, as evidenced in a written agreement, will indicate that the individual is not an employee.

However, there will be parameters in the contractual terms:

- Not be limited in scope (that is, the worker can delegate, subcontract, or assign the entirety of their work to another, as opposed to only discrete tasks)

- Not be a sham, and

- Be legally capable of being exercised.

The Commissioner goes on to state: “Whether the worker is, however, an independent contractor will depend upon an examination of the totality of the legal rights and obligations between the parties.”

It is unclear what the Commissioner means by this. It would appear without doubt that in JMC the weighting to the question of delegation was the substantial factor in favour of characterising an individual as a contractor (independent or otherwise).

- The comprehensive written agreement

A comprehensive written agreement that governs the entire relationship between the parties will be the evidentiary document in considering the employee and contractor divide.

The Commissioner states:

“Where the worker and the engaging entity have comprehensively committed the terms of their relationship to a written contract and the validity of that contract has not been challenged as a sham, nor have the terms of the contract otherwise been varied, waived, discharged or the subject of an estoppel or any equitable, legal or statutory right or remedy, it is the legal rights and obligations in the contract alone that are relevant in determining whether the worker is an employee of an engaging entity.”

Notably, the Commissioner accepts that “evidence of how the contract was performed, including subsequent conduct and work practices, cannot be considered for determining the nature of the legal relationship between the parties”.

Consistent with this, the respective practical compliance guideline (PCG 2023/2) says that there will be low or very low risk outcomes where parties have a written contract expressing the employee v contractor outcome.

- The requirement for written advice

PCG 2023/2 also indicates that each party must commit to and understand the worker classification in their agreement.

The party relying on this classification will fall within the ‘”no risk” or “very low risk” category if they have “obtained specific advice confirming the classification was correct”.

The specific advice does not need to be in writing, but if it is, that will be given greater weighting in the Commissioner’s determination.

Takeaways

The employee v contractor classification is not straightforward.

The High Court’s direction has limited the question to the written agreement (where one is in place). However, issues and disputes between parties regularly arise for “handshake” agreements between friends when the relationship subsequently sours.

The lesson in such matters is simply to get everything in writing.

Phillip London

16 February 2024

accountantsdaily.com.au

Australian Taxation Office (ATO) shifting to firmer debt collection activity

The ATO has flagged a return to more aggressive debt collection actions after seeing a trend of profitable businesses that have the capacity to pay their tax debts but are actively choosing not to do so.

.

The ATO should not be considered as an unsecured lender last in line, because when they lose patience, they hit hard.

Taxed debts include not only income tax, but also unremitted GST and unpaid PAYG withholding, as well as super guarantee charges.

In general, if taxpayers do not pay their tax by the due date or engage with the ATO by the due date to work out a payment plan, general interest charge (GIC) will be applied to any unpaid amounts. GIC is automatically calculated on a daily compounding basis on the amount outstanding and added to taxpayers’ accounts periodically.

What Drives Your Business Growth and Profits?

Every business owner wants to grow their business and their profits.

.

While there’s no secret formula or recipe, the fact is, business growth and improved profitability are outcomes achieved as a result of processes including marketing, your expertise, customer service and your team’s performance.Every business owner wants to grow their business and their profits. While there’s no secret formula or recipe, the fact is, business growth and improved profitability are outcomes achieved as a result of processes including marketing, your expertise, customer service and your team’s performance.

Let’s examine some of the key drivers of growth and profitability.

- Planning – where do you see your business going in the future? What level of profit and growth are you targeting for next year? The definition of insanity in business is doing things the same way and expecting different results. Without a plan to achieve your targets you are just hoping all the moving parts of your business sync together. Unfortunately, hope is not a strategy that delivers growth.

What is your vision for the business and how do you plan to get there? Without a roadmap all roads lead to nowhere. Having a business plan including financial forecasts is really the start of the process because it should identify what resources you need, the equipment and finance requirements. Will you launch new products and services? To achieve the forecast growth, what level of staff will you need?

Another part of the planning process is to complete a SWOT Analysis to ascertain your business Strengths, Weaknesses, Opportunities and Threats. Nobody saw COVID-19 coming but pandemics and snap lockdowns are part of the landscape and you need a contingency plan to deal with such events. As they say, Failing to Prepare is Preparing to Fail.

- Technology has been a game changer in many industries and the rate of change continues to accelerate, just look at what AI is doing and going to do in the future. Before the pandemic arrived a lot of business owners were contemplating some sort of digital transformation to keep up with their competitors and deliver a better customer experience. When COVID-19 arrived, remote working became an urgent priority to keep staff working. Businesses had to invest in technology to help staff transition from office-based to home-based employment and technology that was once considered a luxury became a necessity.

There’s been a massive shift in our daily business habits with face-to-face meetings replaced by video calls on platforms like Zoom, Google Meet, and Microsoft Teams. Going forward, these platforms may well become the default communication method for both internal and external meetings. Travel time has been slashed also but businesses are looking to get staff back into the office. Significant change is afoot again.

Think about what technology you need to speed up your processes, improve productivity, reduce costs and produce better products and services. The right software (local or in the cloud) can save time, help manage your inventory, reduce waste, and generate repeat business with service reminders. It can also automate your marketing efforts. Most importantly, the right digital tools and resources let you keep your finger on the pulse of the business and monitor all the key financial data.

- Marketing – Recent years have seen a significant shift in shopping habits away from retail brick-and-mortar sites such as shopping strips and centres to spending online. The rise of Amazon is ample evidence of this change. With consumers confined to their homes during COVID they became far more familiar with, and keener on, the convenience of shopping online. A trend that has continued after the pandemic. E-commerce sales exploded and this massive shift to online sales is expected to stay for a long time.

To make the most of this shift in consumer behaviour it's time to review your website and, where appropriate, make sure you have an e-commerce store to satisfy customer demand. There are quite a few examples where a business has moved entirely from a retail shop to a totally online model.

Increasing traffic to your site may be as simple as utilising the blog section of your website more effectively. Chances are there is already a blog or news section on your website but nobody is posting anything, or only rarely. If you struggle for what to write in your blog section, head to a question and answer site such as Whirlpool or Quora and find questions related to your industry, product or service and use that question as the title of your blog post and answer the question. Visitors to your site appreciate this content and it will increase the SEO attributes of your website. SEO is important when it comes to Internet searches.

Engaging with your customers in this way and, as well as using social media channels, is no longer optional with your prospects and customers living online. It’s fair to say, for the majority of businesses, your marketing could be the difference between Doom, Gloom and Boom.

- Team – In Michael Gerber’s book, The EMyth Revisited, a key message for business owners was the need to ‘work on the business, not just in the business’. This message should resonate with every business owner and you need to create a business that works independently of you. The purpose of your life is not to serve your business, it’s for the business to serve your life.

Sounds good and easy in theory and the key is finding the right people to run the operational side of the business to free you up. Experienced and trained people who can follow your systems and procedures allow you to delegate tasks you don’t have to do. Rather than manning the sales desk, phones or warehouse you can spend time on the key business drivers like marketing. Wages are often the biggest expense in a business for a reason and their performance can have a massive impact on your growth and profitability. Leadership usually includes managing the team and innovating – that means providing the right tools so the team can perform their tasks in efficiently.

Running a business remains a constant work in progress. To drive better financial outcomes you need to explore ways to continuously improve your business systems and processes. This necessitates planning, the implementation of technology and, today, the adoption of digital marketing techniques. You also need the support of your staff and small improvements can have a compounding effect.

Ultimately the value of a business is linked to factors like revenue, profits and growth rate. It makes a lot of sense to focus on these areas and if you want to discuss the key profit and growth drivers in your business we invite you to contact us today.

ATO’s hands tied with scrapping on-hold debts, expert says

The Tax Office lacks power under current laws to do anything about the wildly unpopular scheme despite plans to review its approach, according to a UNSW professor.

.

Relief for taxpayers with on-hold debts resurrected by the ATO is impossible to achieve without government intervention due to the Commissioner’s inflexible powers, according to one expert.

The ATO announced on Thursday it paused activities around re-raising liabilities previously deemed “uneconomical to pursue” after backlash from the community over the program’s fairness and transparency.

But UNSW associate professor Ann Kayis-Kumar said individuals with on-hold debts hoping for a blank slate would be disappointed because “the ATO’s hands are tied” with no power to write the amounts off.

“The ATO’s in a tricky position. Being responsible for collections and compliance, it needs to walk that delicate balance between collection but also not disproportionately affecting the most disadvantaged in our community,” she said.

“But that raises the question of the discretion available to the ATO.”

Only the finance minister had the power to permanently write off debts owed to the government, she said.

While the ATO could release certain taxpayers’ debts under “serious hardship” provisions contained in the Income Tax Assessment Act, in practice they were ineffective due to being “so outdated and drafted in such a counterintuitive way”.

For example, the current provisions meant the ATO would be less likely to grant hardship relief to taxpayers with more debt.

“That just does not square with reality,” she said. “We need a legislative fix and it really can't be overstated how important that is.”

In the ATO’s statement released yesterday, it announced it would pause the on-hold debts program due to the “frustration” and “concern” caused to the community.

“The ATO has paused all action in relation to debts placed on hold prior to 2017 whilst we review and develop a pragmatic and sensible way forward that takes into account concerns raised by the community,” it said.

However, it said it had “no discretion under the law to waive these amounts and must use any future refund to reduce these debts”.

“In the past, the ATO has excluded some debts from being recovered from taxpayer refunds in this way through long-standing exclusionary criteria, such as for taxpayers on low incomes. However, the Australian Government Solicitor advised this was not in line with the law and so the ATO cannot continue this practice,” it said.

The announcement follows an earlier apology issued by the ATO in November for the “unnecessary distress” caused by its “public awareness campaign” that first alerted taxpayers to the debts a month earlier.

The campaign involved the sending of 200,000 letters to taxpayers and tax agents listing the sums without containing further details of their origins.

Internal documents obtained by The Guardian this week revealed the on-hold debts were the result of the ATO’s gradual removal of filters in its automated systems.

The planned removal of the final filter – debts placed on hold prior to 2017 – would have expanded the program to apply to $15 billion from 1.8 million entities, the documents said.

Ms Kayis-Kumar, who runs UNSW’s pro-bono Tax & Business Advisory Clinic, said on-hold debts disproportionately impacted financially vulnerable individuals without access to tax advice.

Tax agents also reported confusion and increased workloads in attempting to reconcile the debts.

But the community’s concerns could be addressed by giving the Commissioner a “general public policy ground of relief”, in addition to reworking the serious hardship provisions, she said.

A general discretion, as seen in other countries like the US, could allow the flexibility needed to scrap the on-hold debt program in line with public consensus.

“If we adopted something inspired by the public policy ground of relief in the US, the ATO would be able to exercise that discretion in situations like what we’re seeing here,” she said.

“You want decision-makers to be able to make decisions that are in line with community expectations.”

“If we want to see a wholescale improvement to the status quo, we need more reform.”

Christine Chen

23 February 2024

accountantsdaily.com.au

Latest Industry News

THE 2025 FINANCIAL YEAR TAX & SUPER CHANGES YOU NEED TO KNOW!

The new financial year is fast approaching and so are a number of changes to superannuation contribution...

The ATO has developed quite a number of benchmarks to help small businesses develop an idea of their...

ATO’s debts on hold campaign prompts new IGTO guidance

New guidance has been released on best practice principles for debt notifications in response to the...

Illegal access nets $637 million

The ATO has found $637 million of superannuation savings has left the system due to illegal early access...

Countries producing the most solar power by gigawatt hours

Check out the countries that produce the most solar...

Sharing economy reporting regime for platform operators

Individuals participating in the sharing economy should be aware that transactions for supplying taxi...

Why employee v contractor comes down to fine print

The task of worker classification has been a long-running point of contention but the Commissioner’s...

Australian Taxation Office (ATO) shifting to firmer debt collection activity

The ATO has flagged a return to more aggressive debt collection actions after seeing a trend of profitable...

What Drives Your Business Growth and Profits?

Every business owner wants to grow their business and their profits. . While there’s no secret...

ATO’s hands tied with scrapping on-hold debts, expert says

The Tax Office lacks power under current laws to do anything about the wildly unpopular scheme despite plans...

Small businesses may ‘collapse under strain of payday super’, IPA warns

Existing issues within the SG system must be rectified before the government proceeds with the new changes...

Latest Guests News

We are pleased to supply you with the latest edition of Client Alert, which contains information on a number...